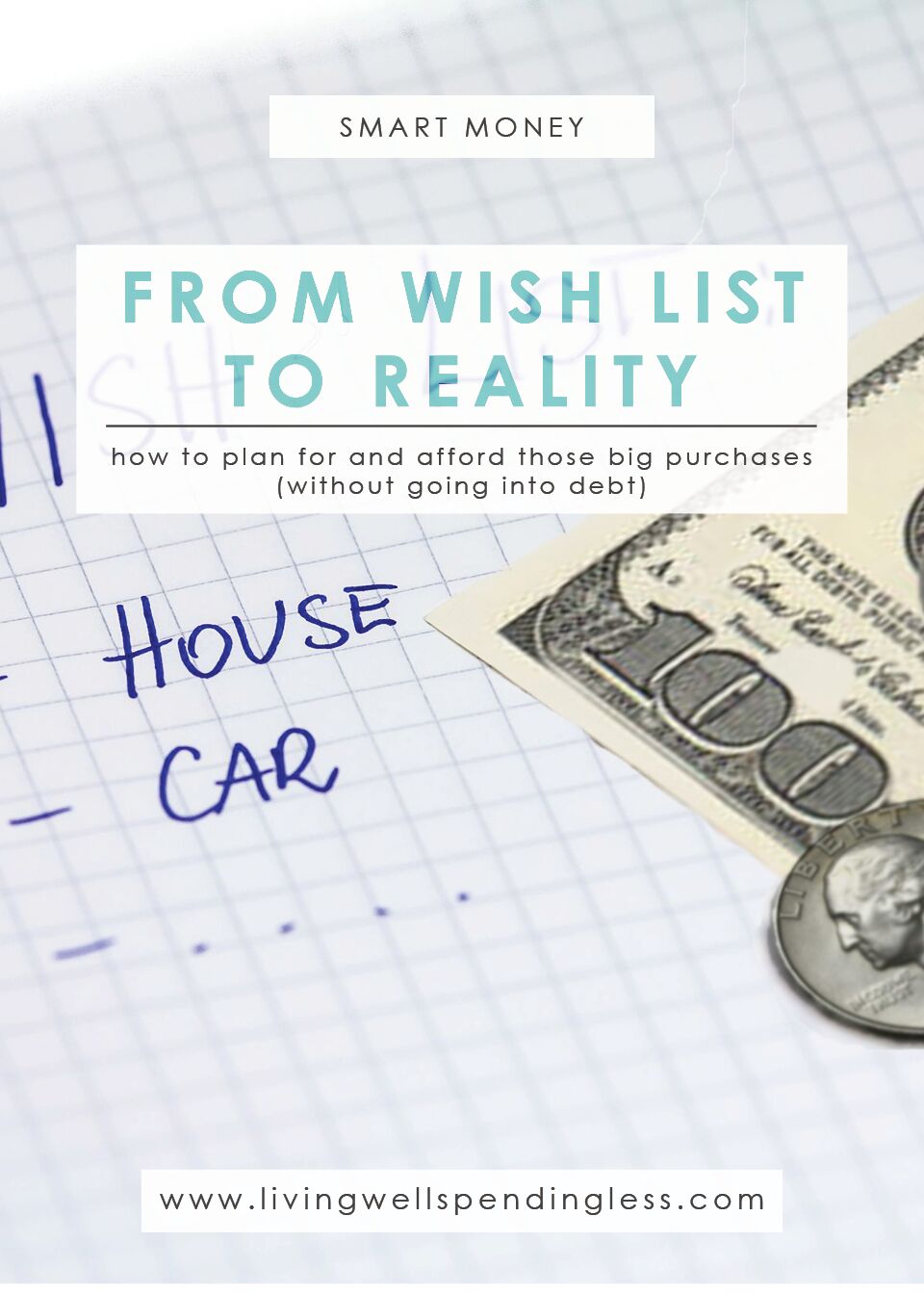

Have you ever wanted something BIG? Something you longed for, even though it was out of reach and (definitely) beyond your budget?

A luxury vacation, a boat, a down payment on a house, a beautiful new piece of furniture, your dream car… Achieving your dreams is possible! With the right mentality and a little bravery, you can get what you want.

The first step? Give yourself permission to dare to think BIG. We only achieve the goals we set out to achieve, so don’t limit yourself. If you want something big, even if it will take five years to save up for it, embrace the wanting—it will drive you.

For years, a friend of mine longed for a Mercedes. Knowing a luxury car was well out of her budget, she decided to start saving anyway. She said, “I knew it would take a long time to save enough, but I really, truly believed that someday I’d get my Mercedes.”

After a few years of strict saving, her Mercedes Fund built up nicely (but it was still looking more like a Toyota Fund). One day, her husband got a call from his uncle. He was looking to unload a “very gently-used Cadillac” for about half the car’s value. She has a teenage son, so they figured they’d shift the cars around so her son would drive her old car and she would drive the Cadillac.

When they got to Ohio to pick up the car, there sat, not the Cadillac, but…a Mercedes.

But this isn’t just a “miracle of the universe” story. Even at half the price, my friend was only able to pay for her dream car in full because she’d already been saving up all those years.

When we allow ourselves to think big and work to crush our goals, we open ourselves up to a world of possibilities.

Many of us get impatient, though. We go out and get what we want on credit, taking on crippling debt that greatly limits our future. We adopt an instant gratification “buy now, pay later” mentality—and it’s bad news for our budgets.

Years ago, people rarely took on debt. If they couldn’t afford a vacation, they simply didn’t go. If they wanted a new car, they’d save up and purchase it outright—even a five-year loan was rarely heard of for such things. Now, instead of calculating our budgets based on saving up for the total cost of an item, we calculate whether or not we can afford the monthly minimum payment.

This way of purchasing is actually much harder on us. It’s like rolling the dice and betting against future financial needs. Life happens. The new car will break down, the boat requires a docking fee, vacation comes and goes…as do sudden trips to the emergency room and calls to a repairman. Suddenly, we might find we’ve fallen down a rabbit hole of insurmountable debt and we have barely a thing to show for it.

It’s not a good place to be.

Instead, let’s shift the instant gratification mentality. Let’s save up for the things we want and need BEFORE we buy them. Not only does this help prevent the accrual of a bunch of interest, but if it’s a long-term goal, we can even earn a little interest back on the money before we buy!

Saving up for big purchases can seem like a BIG goal, but big goals are often the most rewarding when we tackle them. Think of how awesome it will feel when you and your family are sipping margaritas on a cruise ship or hopping into your new ride knowing it’s already paid for. Does it get ANY better than that?

So pick your BIG dream and get started! Here’s how to save up for those wish list items and turn fantasy into reality!

1. Start with a Budget & an Emergency Fund

For big savings goals, the first step before you even consider buying something large is to have a budget AND an emergency fund in place. Need help? That’s okay! The Living Well Planner®features a bunch of easy-to-use, easy-to-follow budgeting and goal setting tools to help you plan for long-term financial success.

In addition to your budget, an emergency fund of around $1,000 is critical. Your emergency fund protects you from taking on more debt when unforeseen “issues” crop up (and they will crop up). Without an emergency fund, life’s little disasters can derail progress.

2. Set Your BIG Goal

Now that your budget and your emergency fund are all set up, it’s time for the fun part: turn your dream into your goal! Write it down and make it real. Research the item or experience you want and calculate out exactly how much it will cost. Have fun with it! Imagine your dream vacation, your new house, or your cool new car!

Let your imagination run wild, but then look at practical ways you can save to reach your goal. Does your new car really need leather seats? Could you get your dream car gently used and a few years older for much less? What are some ways to save on that vacation? You have plenty of time to let your goal evolve and find deals to help you get there.

3. Set the Time frame

So, now you have a goal, WHEN do you want to get there? Are you hoping to hit the ocean for a vacation this summer or could it be moved to off-season when the rates are lower and you have more time to save?

For big goals, give yourself plenty of time. Start saving for a new car while your old car still has some get-up-and-go left in it. When we wait until things are dire or when the goal deadline is right at our doorstep, it can leave us with no other choice but to go into debt for our purchase. We want to avoid that at all costs (even if it means giving up on the goal), so allow yourself plenty of wiggle room to make it to the milestone!

4. Calculate Backwards

You have the amount, you have the time frame, so now calculate out the number of paychecks between now and your goal deadline. If your goal is $2,000, for example, and you want to save it in five months, that’s over ten paychecks at $200 per check. Ask yourself if that’s a realistic goal for you.

This is where you might have to push dates a little further out—would $100 per paycheck be more reasonable? Can you push it out until next summer or next year?

5. Assess Realistically

When setting up your plan, be realistic. What roadblocks do you foresee and how can you plan ahead? For example, if December is often an expensive month with Christmas gifts, can you scale back? Could your family decide to forgo a big Christmas this year to enjoy a vacation in the summer? Giving experiences over gifts rarely results in regret, and is usually much more meaningful.

In addition to any challenges you see, ask yourself if your goal is really worth the sacrifice of what you’ve calculated out. It might be time to go back to the drawing board and find a different vacation destination, a shorter trip or a less expensive piece of furniture. What could you be happy with, that’s still realistic for your family’s goals?

6. Stick to the Plan

Once the plan is in place and you’ve started saving up, the urge to go for it NOW will be strong. Don’t waiver—stick to the plan! Seeing $5,000 in savings can make us consider just buying the car now and financing the other $5,000. (“The payments will be so much less! We’re already used to putting that money aside.”)

This is one of the most difficult parts: not falling off the savings path and going for the gratification now. Be focused on your goal. Think of what you’ll save in interest (and stress) by not taking on more debt to get what you want. Again: stick to the plan.

7. Open a Special Savings Account

It can be hard to transfer the extra money each paycheck—what if you forget, or what if you think, “Oh I’ll spend it now and transfer double next paycheck.” Yikes! If you want to hit a goal, make it automatic. Open a special savings account and have the money transferred in automatically. (Most banks will let you do this for free.) Move it before you even have time to THINK about it. Pretend it’s not even there.

If you’re saving for a long-term goal, like a down payment on a home (something that may take more than a year to save for), ask your bank about opening a CD or another savings vehicle to earn a higher interest on your money. After all, if it’s just going to be sitting there for a year, it might as well be earning for you! Just be sure you can access your money when you want to. Some savings accounts will only let you withdraw once a year or during certain times, or you will accrue a fee (which would defeat the whole point).

8. Go Half with “Extra” Money

What happens when we get a tax refund or sell something we no longer need on Craigslist and earn $100? First, it can be tempting to just think, “Woohoo—free money!” and run out and spend it. But now that you’re a savings pro, that probably doesn’t even cross your mind!

The next impulse is to put that extra money into your goal savings. While this is a great idea and little windfalls can help you tackle goals fast, don’t forget to also continue bolstering your emergency fund and regular savings as well. Put half toward your “goal savings” account and then put the other half into your emergency fund or into your regular savings account. This will help you continue to be prepared for the unexpected, whenever it may arise.

You Reached Your Goal! Congratulations!

Once you’ve reached your goal, it’s time to enjoy it! Go all in and really celebrate the victory! Pat yourself on the back, take tons of photos of you enjoying what you’ve earned and worked so hard for, and make memories that last!

Saving for a big goal is a HUGE victory, and if you do it, you’ll feel like a million bucks when you get there (even if it didn’t cost quite that much). The great thing is that you can save for your dreams without adding to your debt. It’s still possible to get everything you want and enjoy it fully—just set goals and tackle them as you go along!

Aim big and work hard to get there. The reward at the end will be even sweeter!

Ruth Soukup

Latest posts by Ruth Soukup (see all)

- Stop Worrying About Money - July 19

- How to Fit In More Fitness - April 28

- The Most Powerful Decision You’ll Ever Make - April 27

TAKE BACK CONTROL OF YOUR HOME LIFE

Ever feel like you just can't keep up? Our Living Well Starter Guide will show you how to start streamlining your life in just 3 simple steps. It's a game changer--get it free for a limited time!

Ever feel like you just can't keep up? Our Living Well Starter Guide will show you how to start streamlining your life in just 3 simple steps. It's a game changer--get it free for a limited time!

If you love this resource, be sure to check out our digital library of helpful tools and resources for cleaning faster, taking control of your budget, organizing your schedule, and getting food on the table easier than ever before.

This is great advice, but what happens when it is multiple things you want? For instance, currently, we have a savings, checking, retirement and an emergency fund, but what we would like is to replace our shoestring air conditioning units on the house ($15,000) we will be needing a new roof on our house somewhere in the next 3 years ($10,000) and we would like to start making some home improvements like putting in new tile floors in the kitchen and new flooring in the rest of the house ($8,000). All while still trying to contribute to our most important…our retirement fund.

What a great article. I hate having debt of any kind, and always try to pay it off as quickly as possible. And, as you recommend, I try to save for luxuries like trips or a nice car, rather than using credit. I also like to do a lot of research, to make sure I know what I really want, what I’m getting, and what’s a fair price. Finally, before making a purchase, I stop to be grateful for what I already have, and make sure I REALLY need this thing that I’m about to spend my hard-earn money to buy. http://www.homedeconomics.com/spend-less-and-save-more/

Think BIG! That is such good advice! I think I am too the point where I need to start doing that again. I’ve always been a big saver, but life gets monotonous after awhile…I need something big to save for. I don’t want a Mercedes…but maybe I’ll start saving for the Alaskan cruise I used to dream of all the time!

So true, Jennifer. Sometimes I get so busy saving, I forget to spend it on something worthwhile.

And when you have a tough month and still keep at it then find you do have money left after the month you know that you CAN do it….that was my daughters story this month AND then her hubby got a raise which was a fantastic boost.

The advice about working backwards is so important! Thank you for sharing that.

I learned that strategy when I was teaching self-sufficiency classes at a homeless shelter (not to mention learning it myself!) When I actually put it into practice for my website, I got more done in three months than I had the previous year.

I included versions of this theory (through for the free 2017 planner and the budgeting binder) into advice for my own readers.

I love your advice: “When we allow ourselves to think big and work to crush our goals, we open ourselves up to a world of possibilities.”