This is a Guest Post from Cherie at Queen of Free

“I want to rewind today and start all over,” my eight year-old cried out in pain.

“Me, too. Baby. Me, too” I replied.

That evening had started out routinely enough. We picked up a large order from our favorite Thai restaurant to share with our community group. In typical Thursday night fashion, our families mingled together sharing conversation and life updates and kids ran through our legs in and about the kitchen. Eventually, they made their way outside.

The unusually warm late September evening meant they could play freely in the yard, swinging on the swing set, kicking a soccer ball, and chasing each other around in circles. My husband Brian and I sat inside with all but one of the other adults at the kitchen table watching all of the fun while savoring our Pad Thai. Within minutes, the entire world tilted and our lives (and budget) traveled a path we’d never anticipated.

When we saw Zoe fall from the monkey bars, both of us knew it wasn’t good. Brian flew outside in two seconds flat, not even bothering to put on shoes. Hearing her cries, I knew her injury would require more than a kiss on the cheek and the reassuring words “You’re alright.” Upon seeing her arm, I couldn’t immediately tell if was dislocated or broken but I knew it wasn’t good. A dear friend held it in place as we hurriedly laced our shoes and headed to the car. We needed to find the nearest emergency room.

Over the next twenty-four hours, we learned that Zoe broke her arm in two places and fractured it in a third. Due to the proximity to the growth plate, a simple in office re-setting wouldn’t do. She’d need surgery and a titanium nail placed inside to ensure effective healing. It was a whirlwind of tears, IV, consent forms, and very little sleep.

In the weeks that followed, we navigated three different casts and adjusting to a new “normal” where I helped Zoe bathe, tie her shoes, get in and out of the car, and more.

And then the bills began arriving.

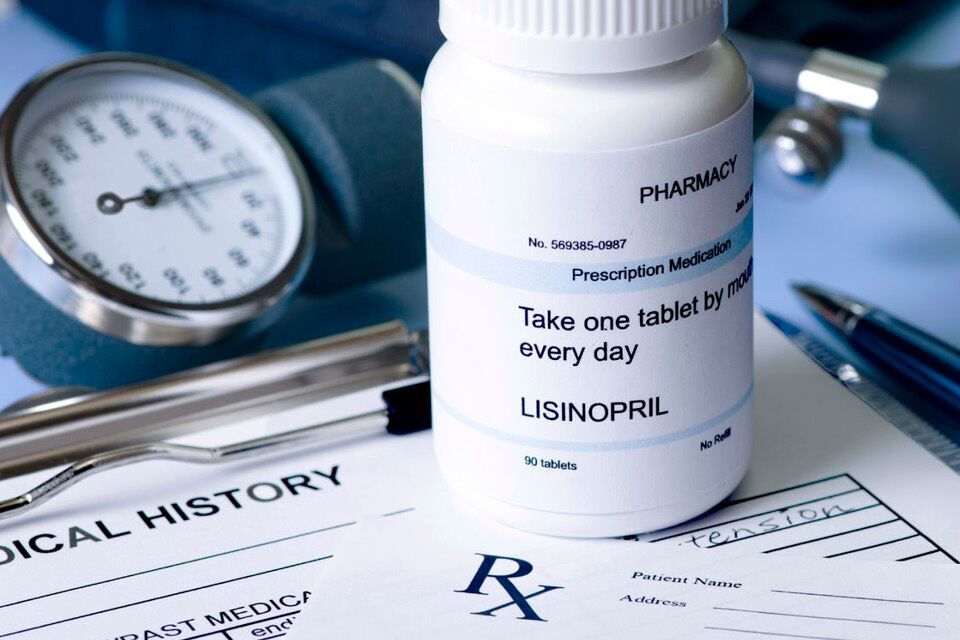

We had gone first to the nearest hospital’s ER and then been transferred a children’s hospital’s ER, and then finally admitted to the children’s hospital. Anesthesia, slings, surgeons, an overnight stay – the bill before insurance was well over $40k. Even after our insurance we were still looking at $10k+.

It was enough to take my breath away.

We had an HSA fund that could cover the majority of the bills. We also had an emergency fund that we could dip into. But we knew there would be at least one more surgery in the next year, too. EOB (Explanation of Benefits) after EOB rolled in, causing my eyes to glaze over. Codes and charges and dates filled each page. Even with a solid knowledge of personal finance, I longed to disengage and wish the entire stack of papers away.

If you’re like me and have faced a similar experience, more than likely, you’ve felt the same sting. Whether planned on unexpected, medical bills can complicate the already overwhelming process of household budgeting and bill pay. When dread fills your heart, take a deep breath. These five simple strategies helped us pay our bills in full and manage a painful physical and financial process.

Avoid the Avoiding

While you may want to close your eyes and ignore the entire situation, you’re doing yourself no favors by setting bills aside and pretending like they don’t exist. When you receive a statement from your insurance company or a bill from a medical provider, open it immediately. Fight the temptation to stick your head in the sand. Read each piece of correspondence from start to finish, making note of any charges you don’t understand.

Create an Organized Information Central

After you’ve opened those bills, don’t just let them collect on the kitchen counter. You need to create an organized system which will allow you to easily access each document when necessary. You may be able to keep everything in something as simple as a file folder, but if you’ve had a major medical emergency, you’ll probably need a banker’s box or expanding file. We used an expanding file to collect all documentation. Organize papers by date received and keep bills from separate institutions in different sections of your filing system. Crack out the paperclips and the Post Its. It’s time to get those medical bill ducks in a row.

Log Every Communication

More than likely, you’ll need to reach out to a representative of either your insurance company or medical service provider. Remember those notes you took on line items you didn’t deserve? Each time you speak to someone, carefully log the date, the time, the name of the individual you spoke with, and what you were told. Wading through working with insurance companies, doctors, and medical facilities is more than likely going to take you months. You need a clear record of who said what and when in case there’s ever any confusion.

Ask Questions and for a Discount

Again, don’t ever hesitate to ask a customer service representative to clarify charges or why the insurance company did not choose to cover a specific fee. If someone can’t give you a coherent answer that makes sense to you, then ask for a manager and repeat your questions.

Many hospitals and medical billing companies will give you a discount if you pay the sum in full. We were able to save 10% on two fairly hefty bills by asking if there was a price break for this payment method. It saved us well over $500 in the end.

If you can’t make a lump sum payment, your provider may allow you to set up an interest free payment plan to break up the total amount over several months.

When Necessary, Appeal

It’s extremely important to crack out your policy – either in digital or paper format – and read it carefully. If it seems like perhaps your insurance company should have covered a charge it didn’t and you know your policy well, write a letter of appeal.

As we read our policy and waded through what should have be covered for Zoe’s trips to two ERs, we realized over $6k had been denied. We fully believed as the policy stated they should have been paid. So, carefully we crafted a letter that clearly laid out the finer points of the policy. We had no guarantee that the company would agree with our evaluation but it was worth the try. If you feel like you’re not capable of writing a clear letter, ask a friend to help you.

You can imagine our relief when we received a reply stating our appeal had been granted and they planned to cover the cost in full. It was certainly worth the time spent evaluating our policy and penning the request. Even still, we had to carefully monitor that the payment was actually sent to the providers (there were two separate bills). It took two to three months and several phone calls, creating a very lengthy communication log. But in the end, checks were cut for both providers and we closed that portion of our file.

At times, tracking the expenses, communicating with the medical providers and insurance company felt like a part time job. However, the time we spent was well worth our efforts to the tune of thousands of dollars.

Doctors’ or hospital bills don’t have to derail your financial goals. And while no one wants to go through the pain of an illness, a broken arm, or unexpected hospitalization, you can still come out on the other side of the experience with your bank account intact. Take a deep breath and good records. You’ve got this. It might take time, but meticulously dealing with the details might help you save hundreds or even thousands of dollars.

Cherie Lowe is an author, speaker and hope bringer. Her book Slaying the Debt Dragon details her family’s quest to eliminate over $127K in debt in just under four years. As her alter ego the Queen of Free, Cherie provides offbeat money saving tips and debt slaying inspiration on a daily basis.

TAKE BACK CONTROL OF YOUR HOME LIFE

Ever feel like you just can't keep up? Our Living Well Starter Guide will show you how to start streamlining your life in just 3 simple steps. It's a game changer--get it free for a limited time!

Ever feel like you just can't keep up? Our Living Well Starter Guide will show you how to start streamlining your life in just 3 simple steps. It's a game changer--get it free for a limited time!

If you love this resource, be sure to check out our digital library of helpful tools and resources for cleaning faster, taking control of your budget, organizing your schedule, and getting food on the table easier than ever before.

This is so hard! I remember breaking my arm as a little girl and can only now think off all my mom went through.

Budgeting for medical surprises I think is the hardest part of a families finances. But I am glad to hear that they covered it in full!